Major Update for First-Time Buyers: Save Up to $50,000 on GST for New Homes

There’s big news for Canadians looking to enter the housing market.

The federal government has officially passed the Making Life More Affordable for Canadians Act which introduces new legislation aimed at improving affordability for first-time buyers by offering significant GST savings on newly built homes. For many buyers, this could mean keeping tens of thousands of dollars in their pocket when purchasing a new construction property.

At our brokerage, we’re already working with clients to understand how this program applies to their situation, and more importantly, how to structure their purchase to fully benefit from it.

What’s Changing?

Under this new program, eligible first-time buyers may qualify for a full or partial rebate on the 5% GST applied to newly built homes. The amount of the rebate depends on the purchase price.

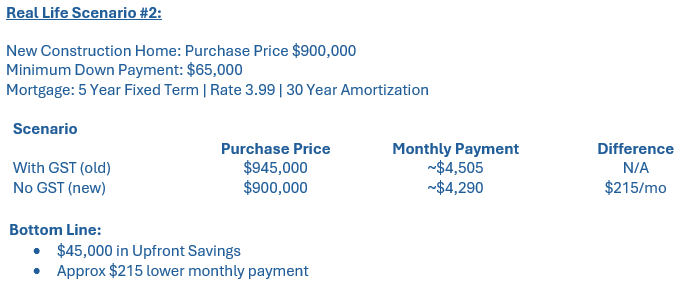

Homes priced at $1,000,000 or less may qualify for a full rebate, representing potential savings of up to $50,000. For homes priced between $1,000,000 and $1,500,000, a partial rebate may still be available, calculated on a sliding scale. Properties above $1,500,000 are not eligible under this program.

It’s also important to note that this rebate is separate from existing federal and provincial programs, meaning buyers may be able to layer multiple incentives to further improve affordability.

Why This Matters Right Now

For buyers considering a new build, this program can have a meaningful impact, not just on the purchase price, but on how the entire transaction is structured and ultimately a buyers overall purchasing power.

How We Help You Navigate This

With any new government program, there’s always a window where the opportunity is clear but the details are still evolving. Understanding when the rebate is applied, how it affects the mortgage amount, down payment and closing cost is why working with an MMG Mortgage Broker is paramount.

Our role as a mortgage brokerage is to help first-time home buyers navigate that uncertainty with confidence. We work closely with buyers, builders, and real estate professionals to make sure everything is aligned from the start. That means helping determine whether you qualify, estimating your potential savings, and structuring your financing so the rebate is properly accounted for, especially in cases where it may be applied upfront.

We also help you plan for the full picture, including deposits, closing costs, and cash flow, while coordinating with your builder and lawyer as more guidance is released. The goal is simple: to make sure you’re not just eligible for the program but well positioned to benefit from it in a meaningful way.

Who Qualifies?

To be considered a first-time home buyer under this program, you must be at least 18 years old and a Canadian citizen or permanent resident. In addition, you cannot have lived in a home that you, or your spouse or common-law partner, owned in the current year or the previous four calendar years.

Important Timing Considerations

The rebate is expected to apply to agreements entered into on or after March 20, 2025. However, there is still some uncertainty around whether eligibility will be determined based on the date the purchase agreement was signed or when it became unconditional.

Final clarification will come from the Canada Revenue Agency (CRA), and we are actively monitoring updates so our clients can make informed decisions at the right time.

Already Purchased a New Build? You May Still Benefit

If you’ve recently purchased a newly built home, you may still be eligible depending on your timeline.

Buyers who purchased after March 20, 2025 and have already taken possession (prior to March 12, 2026) may be able to apply for the rebate once the official process is released. In these cases, the application would be submitted directly by the buyer.

For those who have signed a purchase agreement but have not yet taken possession, there may be an opportunity for the rebate to be applied directly to the purchase price. This could reduce the amount required at closing, rather than waiting to claim the rebate afterward. As details are finalized, we help ensure your financing is structured accordingly so everything lines up.

*Canada Revenue Agency (CRA) has released the required forms here with additional information found here.

Thinking About Buying a New Build?

This is one of the more impactful affordability programs we’ve seen in recent years and how you approach it matters.

Whether you’re actively looking or just exploring your options, we can help you understand how this rebate fits into your budget, what price range makes the most sense, and how to structure your mortgage to take full advantage of the opportunity. Just as importantly, we help you avoid common pitfalls as new program details continue to roll out.

If you’re considering a new construction home, or wondering if your recent purchase qualifies, now is the time to take a closer look.

Have questions or want to run your numbers?

Reach out to our team and we’ll walk you through how this program could apply to your specific situation.