Team |

Apply |

Services |

Insurance |

Company |

Calculators |

News |

Contact

Back

Products & Services

Renewals

Investment Property Financing

Acreage Financing

Build

Land

MLI Select

Credit Knowledge

Pre-Qualifications

Bank of Canada Announcements

Home Protection Warranty

Back

All About Insurance

Get A Quote!

Back

Social Contract

Reviews on Google

Reviews on Facebook

Charity

Team |

Apply |

Services |

Products & Services

Renewals

Investment Property Financing

Acreage Financing

Build

Land

MLI Select

Credit Knowledge

Pre-Qualifications

Bank of Canada Announcements

Home Protection Warranty

Insurance |

All About Insurance

Get A Quote!

Company |

Social Contract

Reviews on Google

Reviews on Facebook

Charity

Calculators |

News |

Contact

Scroll

Specializing in all types of property financing.

APPLY NOW!

What Our Happy Clients Say

Reviews on Google

Reviews on Facebook

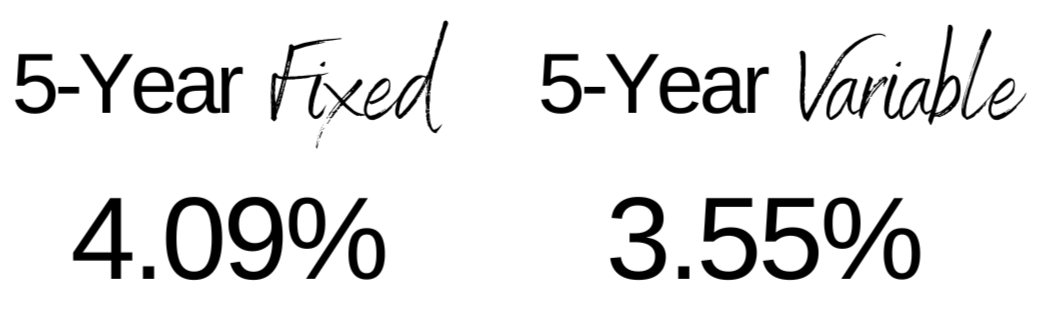

INTEREST Rates

The lowest rates are not always the best options or available options!

Interest rate is dependent on down payment, credit score, amortization, closing date and lender.

Our advertised rates are fully featured with NO Restrictions!

Email Us For More Information

10-Year Fixed

5.49%

7-Year Fixed

5.14%

4-Year Fixed

4.14%

3-Year Fixed

3.94%

2-Year Fixed

3.94%

1-Year Fixed

4.54%

intro

What Our Clients Say

Rates

Chat with us

, powered by

LiveChat